Industries

Trade Credit Insurance

What is Trade Credit Insurance?

Trade credit insurance insures manufacturers, traders and providers of services against the risk that their buyer does not pay (after bankruptcy or insolvency) or pays very late.

The trade credit insurance policy will pay out a percentage of the outstanding debt. This percentage usually ranges from 75% to 95% of the invoice amount, but may be higher or lower depending on the type of cover that was purchased.

In the absence of trade credit insurance many trade transactions would have to be done on a pre-paid or cash basis, or not at all. It is an essential credit management tool and used to control risks, improve payment behaviour, obtain vital buyer information, and monitor exposures.

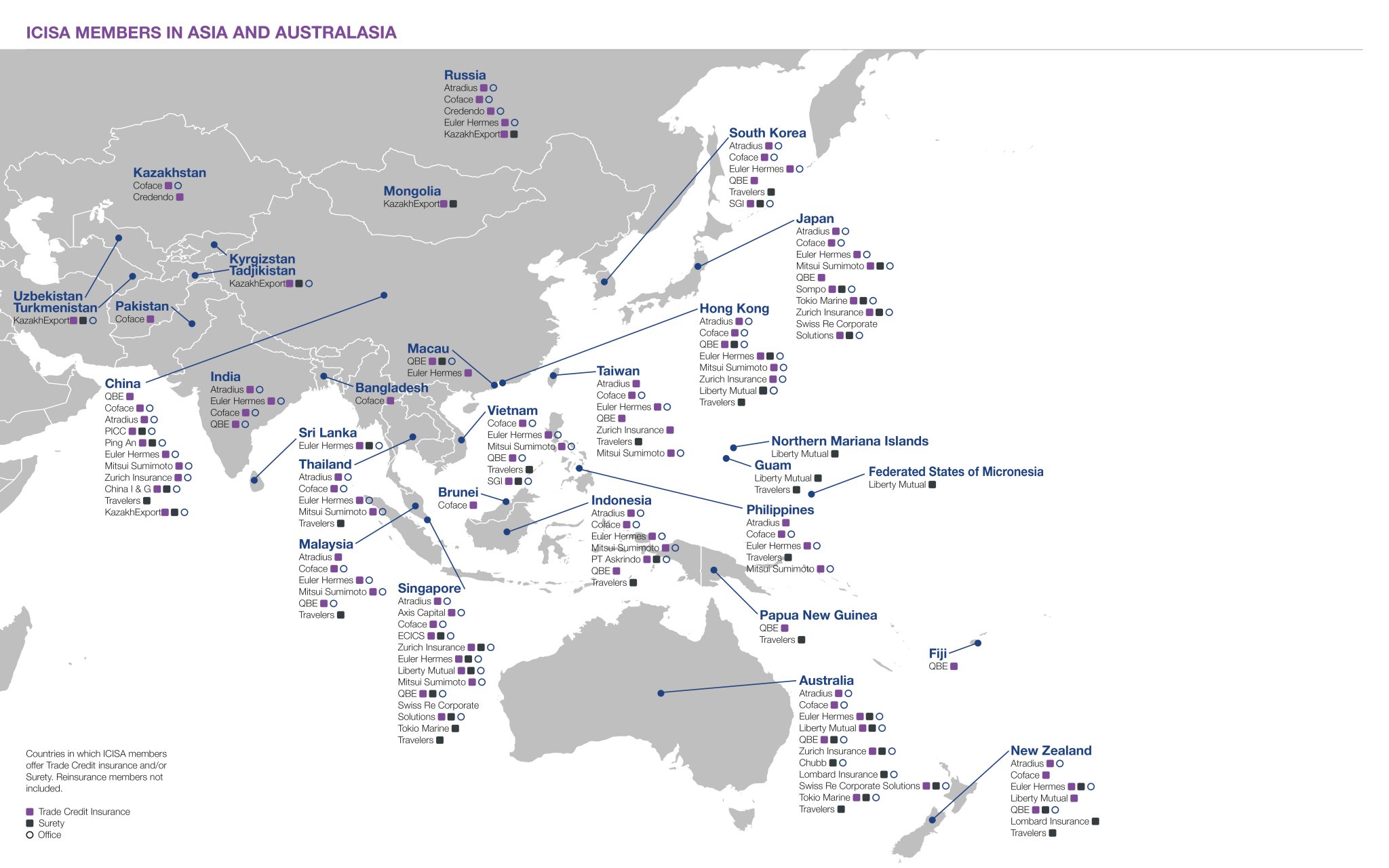

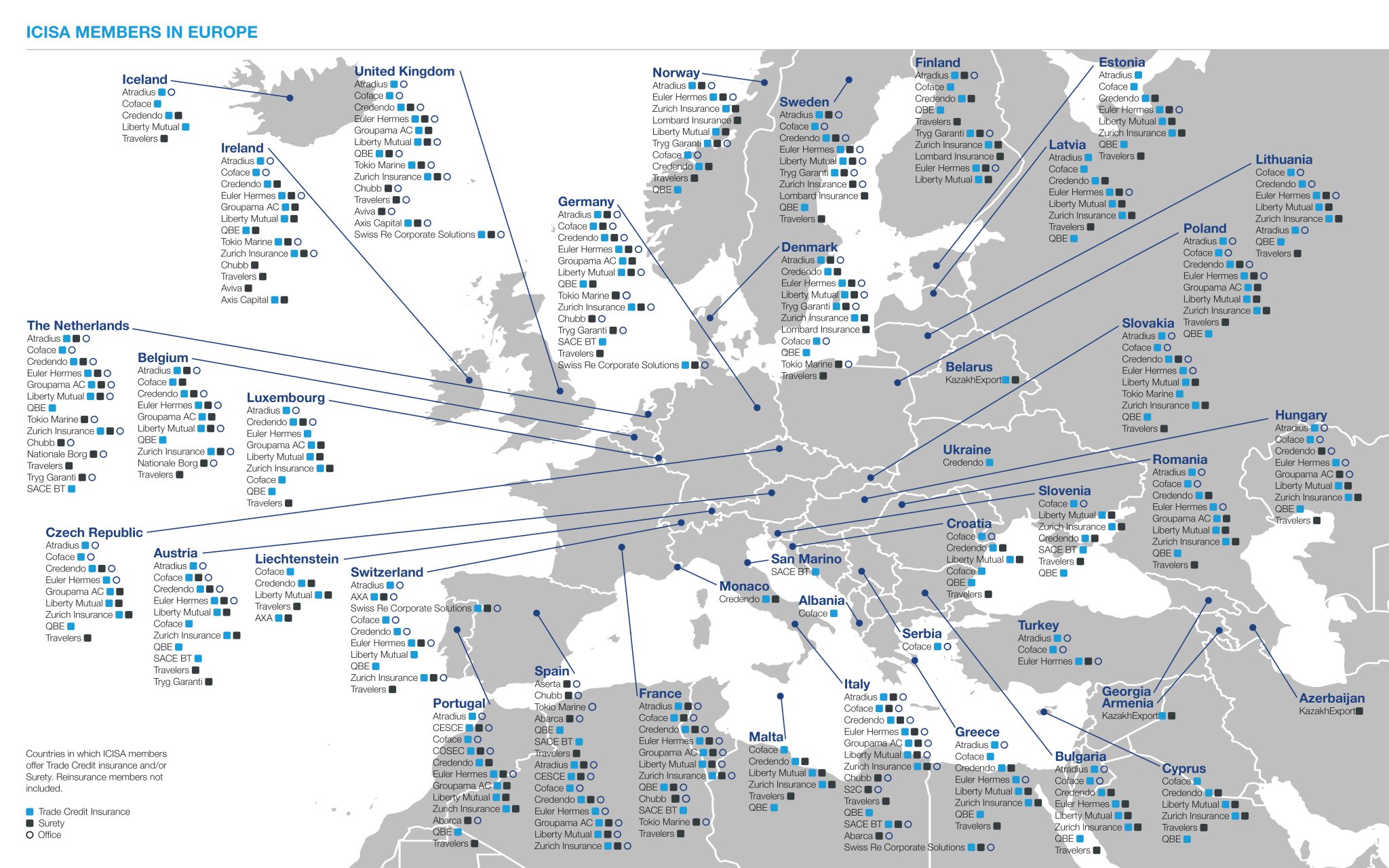

Where is TCI available?

Here is an overview of countries where ICISA’s trade credit insurance and surety members offer their products. Click on each picture to see it on better resolution.

Glossary of TCI terms

Trade credit insurance protects businesses against the risk that customers’ are unable to pay for products or services. This can be because of bankruptcy, insolvency, or political upheaval abroad.

FAQ

Below you will find frequently asked questions on TCI related topics. If you have any additional questions please feel free to contact secretariat@icisa.org.

General Information

Trade credit insurance insures manufacturers, traders and service providers against the risk that their buyer does not pay for the goods delivered or services provided to them due to insolvency(or a similar legal status) or pays very late, respectively does not pay after an agreed number of months after due date (Protracted default). Insolvency cover and protracted default cover together are also referred to as the commercial risk.

It may also insure political risk, i.e. the risk of non-payment by foreign buyers due to currency issues, political violence, confiscation, expropriation,nationalisation or deprivation, etc.

The policy is taken out by the supplier and in the event of a claim (unpaid invoices) the policy pays out a percentage of the outstanding debt owed to them. This percentage usually ranges from 75% to 95%, depending on the type of cover that was purchased.

Trade credit insurance policies are flexible and allow the policyholder to cover the entire portfolio or just the key accounts against above mentioned risks. The most common type of cover is so-called Whole Turnover Cover, which covers all buyers of the policyholder.

It is a business enabler – in the absence of trade credit insurance many trade transactions would have to be done on a pre-paid or cash basis, or not at all.

It is an essential credit management tool and used to control risks, improve payment behaviour, obtain vital buyer information (which, is especially for new buyers, of high importance), and monitor exposures. Credit insurers have large and up-to-date data bases regarding buyers and payment behaviour.

When late payment occurs credit insurers can step in and provide a collection service, hence the insured gets quicker its money and protects its liquidity. Due to its debt collection services final losses are typically reduced and can sometimes even be avoided.

A credit insurance policy helps the supplier obtain external financing, since it can be assigned to the financing bank or to a factor as a security.

A trade credit insurance policy can also reduce bad debt provision and reduces its Expected Credit Loss according to IFRS9.

The credit risk that is insured must have a direct link with an underlying trade transaction, i.e. the delivery of goods or services. If no such direct link exists, the outstanding amount is not insurable under a trade credit insurance policy.

To be insured, transactions must not be subject to disputes. Parties are usually requested to resolve any dispute, prior to involving the insurer.

Since January 2018, businesses reporting under the International Financial Reporting Standard (IFRS) are required to adapt their trade receivables impairment process to the new IFRS 9 regulation.

This new accounting standard results from the need for more accurate and reliable accounting methods and better risk prevention. As such, companies should move to a predictive impairment model, by switching from incurred loss to Expected Credit Loss (ECL) for all trade receivables.

A trade credit insurance contract will allow the policyholder to reduce its Expected Credit Loss due to the anticipation that the trade credit insurer will pay an indemnity in case of default of the Buyer allowing the policyholder to substitute the probability of Default (PD) of the Trade Credit insurer to the buyer’s PD.

Some trade credit insurers also provide IFRS 9 product to help companies to determine the Expected Credit Loss with less volatility and robust methodology.

Suppliers / sellers of goods or services. These can vary from small and medium sized enterprises (SMEs) to multinational companies. Banks or financial institutions can also seek credit insurance cover to secure trade receivables they own though financing agreements.

All trade credit insurers offer information on their products through their websites. Often policy wording or non-binding quotes can also be obtained on-line. Custom made quotes and policies can be obtained either on-line or directly from the insurer. Brokers, in particular specialised brokers or brokers with a specialised trade credit insurance department, also offer non-binding indications upon request.

Insurers have different ways of insuring receivables. Policy holders can often choose smaller or larger risk sharing options. Policies that are currently offered can cover domestic sales as well as worldwide sales, depending on the wishes of the customer. Customers can often choose between insuring a single transaction or all their sales. The bad debt record of the policyholder, plus the predictions for the sector and the economy are factored into the pricing. All these factors influence the premium rate widely. This insurance-type is quoted on the basis of standard actuarial techniques. It is sold mostly on a whole turnover basis and premium rates are generally given as a percentage of the company’s turnover (including financially sound and weak customers). Due to the unknown nature of future turnover, a minimum premium amount is usually an integral part of the contract. Insurers offer a free quote without any obligation, either on-line or from dedicated sales staff.

The maximum liability amount is used to limit the loss that can be sustained through one single policy, hence also called policy limit. If the total loss of a policy occurring in one year exceeds the amount of the agreed maximum liability, the actual claim payments for this policy is limited to this amount. The maximum liability is often defined as a multiple of the earned premiums in a given policy contract.

Credit insurers offer various standard policies, which have been developed for different policyholder segments (e.g. SME, multinational corporates) and industry segments (e.g. for construction, energy, transport or recruitment , etc.). These can be adapted to specific individual circumstances.

A trade credit insurer will always investigate your particular circumstances and wishes. The result is a tailor made policy at a corresponding affordable premium.

Outstanding receivables are usually the largest or second largest item on a trading company’s balance sheet. Bad debt losses can affect liquidity and profits. Even worse, it could result in a company’s financial ruin. Late payments or non-payments therefore pose a considerable threat to future liquidity of that company if no measures are taken. By insuring these receivables against non-payment or late payments, the company ensures its cash flow. Companies that have their business financed by a bank can assign their trade credit insurance policy to their bank as a security.

Mastery of sophisticated financial analysis and data management techniques are key success factors in trade credit insurance, as is global-scale service provision. Multinational trade credit insurers have local teams based throughout the world to evaluate the financial position of buyers worldwide on a daily basis.

The risk is diluted through insurance techniques and risk sharing, by moving a larger or smaller part of the risk to a reinsurer. Insurance techniques are used to mitigate the risk and avoid moral hazard & adverse selection. These include assuring an adequate spread, regionally as well as over sectors, dynamic risk management, agreed maximum liabilities as well as risk sharing agreements and debt collection.

A trade credit insurance policy is a conditional insurance contract between two parties that cannot be traded. A financial guarantee is unconditional, usually on-demand, and transferable.

A trade credit insured risk is always directly related to an underlying trade transaction, which is either the delivery of goods or of services. The correct fulfilment of this trade transaction is essential for trade credit cover to exist.

A financial guarantee is independent and does not rely on any third contract.

Differences between Domestic and Export trade credit Insurance and factoring

Domestic policies cover trade with buyers situated in the policyholder’s own country. Political Riskis not insured in domestic policies.

Export policies cover trade with buyers situated abroad i.e., outside of the policyholder’s own country. Export policies may include political risk cover in addition to commercial risks cover. For many years, cover has been available from the private market for both commercial as well as political risks. Policies covering export debts can be more expensive due to the increased scope of cover which can involve longer periods of time.

By having export credit insurance cover, a business can have confidence to trade on credit terms in markets where credit terms may not normally be offered, especially with buyers who less known to the seller. It also removes the need for expensive Letters of Credit.

Businesses can insure their domestic and export credit risks in one single policy. In the case of multinational traders, this is of particular value as the distinction between export and domestic risks is often irrelevant for these enterprises.

A domestic credit insurance policy covers the payment risks from buyers that are established in the same country as the policyholder. Domestic policies do not include political risk cover.

Trade credit insurers insure against the risk of non-payment. Most insurers also offer additional products, such as debt collection services, buyer/country rating, portfolio assessment and securitisation cover.

Factoring is not credit insurance but is a finance product where a business can fund their cash flow by selling their invoices to a third party at a discount. A factoring company buys receivables. It may also be used to outsource some of the activities of the credit department. The purchase of receivables ensures payment at a fixed date and makes it possible for companies to fund all or some of their invoices and thus cover their operating capital requirements; obtain payment of receivables with shorter payment terms; outsource or vary their administrative expenses; and optimize current assets and liabilities.

Factoring companies do not usually bear the risk of non-payment and as a consequence either the funding would be reversed and the account debited in the event that the buyer does not pay the receivable, or factoring companies partner with trade credit insurance companies to obtain a policy to cover their customers against the insolvency of their buyers, according to the type of factoring agreement (with or without recourse). A factorer may purchase credit insurance which the business can benefit from on either a selective or whole turnover basis.

Credit Limits

The trade credit insurer issues a credit limit for every buyer with whom the policyholder trades (except otherwise provided in the policy). The credit limit is requested by the policyholder using the credit insurer’s form or online tool. The level of the limit to be requested should be the amount that the buyer will owe to the policyholder. The trade credit insurer will then assess the request and if the underlying information justifies cover they will approve the limit in full or at a restricted amount. The granted credit limit (which may be a nil limit) is the maximum insured cover for a specific buyer and the policyholders can trade on an insured basis within the approved credit limit throughout the policy period without further reference to the insurer.

If a discretionary limit has been agreed in the policy, exposures up to that amount do not have to be agreed by the trade credit insurer but are covered based on specific rules defined by the trade credit insurer such as the purchase of an information report on the buyer from an information provider or the payment experience of the policy holder with his buyer.

The trade credit insurer has the right to reduce or cancel a granted credit limit at any time, usually as a result of negative information. This allows the policyholder to bring down its exposure in a timely manner, as negative news (such as deterioration in payment behaviour) is known immediately. The new limit will apply to all deliveries that are made by the policyholder to the buyer after the date of the trade credit insurer’s decision to reduce or cancel a limit.

Trade credit insurers are not always aware of the identity of all the insured buyers (specifically the smaller ones). Policyholders are normally given a discretionary amount up to which they may trade under the cover of the policy in compliance with the discretionary limit rules without notifying the insurer. Any exposure exceeding this discretionary amount is submitted to the trade credit insurer’s underwriter and confirmed by the trade credit insurer through a written credit limit.

Trade credit insurers are not always aware of the exact usage of the granted credit limits, although average usage is known, and high-risk exposures are actively monitored.

On a case by case basis, to better steer the exposures, the trade credit insurer may ask the policyholder about its current usage of the credit limit.

There are different definitions of credit management which usually include assuring that buyers pay on time, credit costs are kept low, and poor debts are managed in such a manner that payment is received without damaging the relationship with that buyer. A trade credit insurance company does all that through prevention on the buyers and debt collection services, either directly or in conjunction with a company’s credit department. An approved credit management policy can offer assurances to a financing bank, which may facilitate financing.

Suppliers that deliver goods and/or services on credit have to manage this credit risk to ensure that payment is received on time. Several tools come to the aid of today’s credit manager. These can be used as additional security to existing credit management procedures. If no procedures are in place, these tools can assist in setting these up. Trade credit insurance is a package of tools offered to the credit managers including assessment and monitoring of the buyer, debt collection and indemnification of unpaid debts.

One of the most important credit management tools is reliable up to date buyer information. A supplier only sees one side of his buyer. Independent information is essential for efficient credit management. A trade credit insurance through the prevention process provides monitoring and updates on the buyers.

A buyer may be sound, but the country he is in may be experiencing problems. Country reports detect trends and alert exporters before serious problems arise in a particular country that can affect the buyer.

Types of policies and who is covered

A whole turnover trade credit insurance policy includes all buyers and insures against non- payment by the buyer. Because of the spread of risk, premium rates are usually competitive. The entire buyer portfolio is constantly being monitored, and suppliers are advised about the state of every buyer.

Companies that are generally not worried about not getting paid may still have a few large risks that can cause concern in case they cannot or will not pay. Trade credit insurance policies can be tailor made to cover only those exceptional buyers, e.g. through high thresholds or retentions, without including every receivable the company has.

Yes, this type of cover is particularly useful for companies that deal with only one buyer or have very few transactions.

Multinationals want to benefit from their buying power. They look for seamless cover across borders, yet with local service in local currency and local language. Multinational trade credit insurance programmes are offered by many trade credit insurers and provide just that. They may include a single wording with policies issued in different languages and/or currencies to suit the needs of the different subsidiaries.

Many trade credit insurers offer policies aimed at small and medium sized enterprises (SMEs), which contain simple language, are competitively priced, and have low administration. These policies are typically available on-line directly from the insurer.

Political Risk (PRI)

The risk that a buyer cannot pay or that goods cannot be delivered due to circumstances outside of the policyholder or the buyer’s control. These circumstances typically include “CEND” (Confiscation, Expropriation, Nationalisation, Deprivation) and “Contract Frustration” (e.g. non-payment by a public buyer, non-transfer of currency, currency inconvertibility). Policies may also include coverage of War or Political Violence (e.g. Terrorism, Strikes, Riots, Civil Commotion).

Yes, many trade credit insurance companies offer comprehensive cover as part of their standard policy, i.e. political risk can be included in the coverage alongside commercial risk.

Civil unrest is generally not considered to be part of Political Risk but rather of Political Violence (PV). Payment by a buyer however can be obstructed as a result of strikes, protests or other civil unrest. Therefore, it may be included as an additional cover in a comprehensive Trade Credit insurance policy or PRI policy.

A change of government in the country of the buyer may lead to a change in politics. If the buyer was nationalised, its payment obligation might subsequently be cancelled. Payment can be insured through Political Risk cover.

The risk or the inability to transfer money from one country to another, and therefore, for not getting paid can be insured under Political Risk cover.

War and terrorism are generally not considered to be part of Political Risk. Payment by a buyer however can be obstructed as a result of war or terrorism. Therefore, one or both of these risks may be included as an addition to a comprehensive trade credit insurance policy or PRI policy.

The term “marketable risk” refers to those risks that are covered by commercial trade credit insurance companies without the support of a government or state. In the European Union, they are not permitted to be covered by state-sponsored export credit agencies (ECA). In turn, non-marketable risks are those risks for which no cover is available in the private market. Trade credit insurers determine their position on each country based on the economy, stability, currency and payment statistics.

A small number of countries is considered non-marketable, mainly because of war, “failed economies”, and increasingly also due to sanctions. Therefore, those countries are typically off cover. Country risks are reviewed continuously, which can result in changes that may turn previously non-marketable risks marketable and marketable risks non-marketable.

The underlying risks are clearly different (politically imposed vs. commercial triggers), however the insurance policy may be tailored to combine the two according to the requirements of the policyholder’s business for export risks.

Non Payment and Claims

There are three main reasons why a buyer does not pay –

- insolvency occurs

- a buyer cannot or will not pay but they still exist (protracted default)

- a political risk event occurs

Depending on the scope of the credit insurance policy all three of these instances can be covered by trade credit insurance. Each policy will define the claim events and claim payment timescales.

Insolvency (or its equivalent depending on the jurisdiction) is a formal legal process for companies who have insufficient assets to cover their debts and are unable to honour their financial obligations or repay their debts. The process begins when a petition is filed and, from that point onwards, is overseen by an official who will measure the company’s assets and determine what funds can be distributed to the creditors.

Normal payment obligations cease when a buyer is declared insolvent, an administrator or receiver is appointed, is put into liquidation or a bankruptcy protection period is announced.

A common reason for not getting paid is that a buyer goes into insolvency before payment is made.

Insolvency, or its equivalent depending on the jurisdiction, is a recognised cause of loss on trade credit insurance policies and triggers the start of the claims process. The policy will stipulate how quickly insolvency claims will be paid – normally this is within a month.Buyers sometimes opt for an insolvency protection arrangement, also known as Chapter 11 in the USA and under different names in other jurisdictions. Such an arrangement gives the buyer protection to delay payments for an extended period while they file a plan to reorganise their business, debts and assets.

This occurrence is considered a claim event and is covered under a credit insurance policy. The policy will stipulate the period before the claim can be paid.

If a buyer is late in paying their debts, an established collection procedure is called for. Most companies have internal guidelines on how to deal with late payers. However, sometimes these efforts do not have the desired effect.

In these instances, it can be helpful to employ a professional collection agent. Standard approaches for recovery may include telephone calls, written demands, and visits to the buyer’s premises. A debt collector can give advice on how they think it will be most effective to collect a debt, this could include agreeing a formal repayment plan with the buyer.

Most trade credit insurance companies either offer an inhouse debt collection service or have partnered with specialised collections firms. Depending on the trade credit insurer this may be optional or a compulsory part of the policy.

Pro-active debt collection procedures have a high success rate. A buyer may be in difficulty, but the supplier can still control payments, provided professional debt collection procedures are in place. Most trade credit insurance companies either offer inhouse debt collection services or have partnered with specialised collections firms.

Protracted default is when a buyer cannot or will not pay, but they have not gone into insolvency. Credit Insurance policies often offer cover against protracted default.

The credit insurance policy will stipulate how much action to collect the debt needs to be taken before Protracted Default is deemed to occur, this may include instructing a debt collector or issuing court proceedings. There will also be a pre-determined period before the claim can be paid (normally a waiting period of up to 6 months). By offering protracted default cover it means the policyholder can claim sooner as they don’t have to wait for insolvency to occur.

Depending on the trade credit insurer once a protracted default claim has been paid, the trade credit insurer may become subrogated on the debt and as such can make decisions on how to pursue the buyer for payment.

The underlying risks are clearly different (politically imposed vs. commercial triggers), however the insurance policy may be tailored to combine the two according to the requirements of the policyholder’s business for export risks.

Our book: A guide to trade credit insurance

‘A Guide to Trade Credit Insurance’ is a reference book on trade credit insurance, written from an international perspective. It is a compilation of contributions from various authors and reviewers drawn from ICISA member companies.

Any questions on the topic?

If you want to know more about this topic, feel free to contact us.