Industries

Surety

What are Surety Bonds

Bonds and guarantees are normally required under the terms of a construction or engineering contract, or in accordance with mandatory legal requirements, to secure the obligations of the principal debtor (generally known as the principal) against the beneficiary.

They guarantee the performance of a variety of obligations, from construction or service contracts, to licensing and to commercial undertakings. Almost any sale, service or compliance agreement can be secured by a surety bond.

A surety bond is an agreement, issued by an insurance company, which (in most cases) provides for monetary compensation in case the principal fails to perform. Although many types of surety bonds exist, the two main categories are contract and commercial surety.

For more information, please visit the surety Frequently Asked Questions.

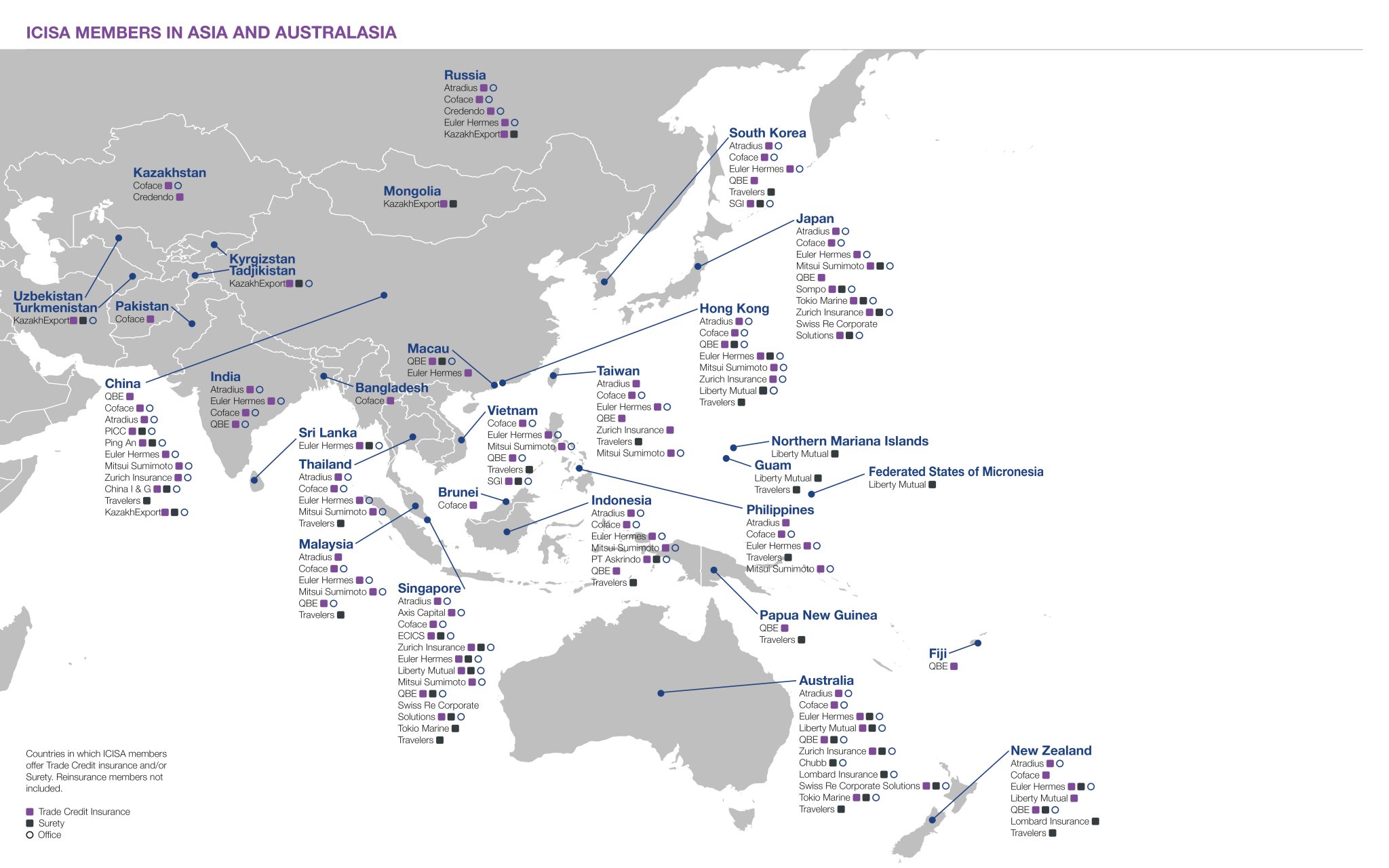

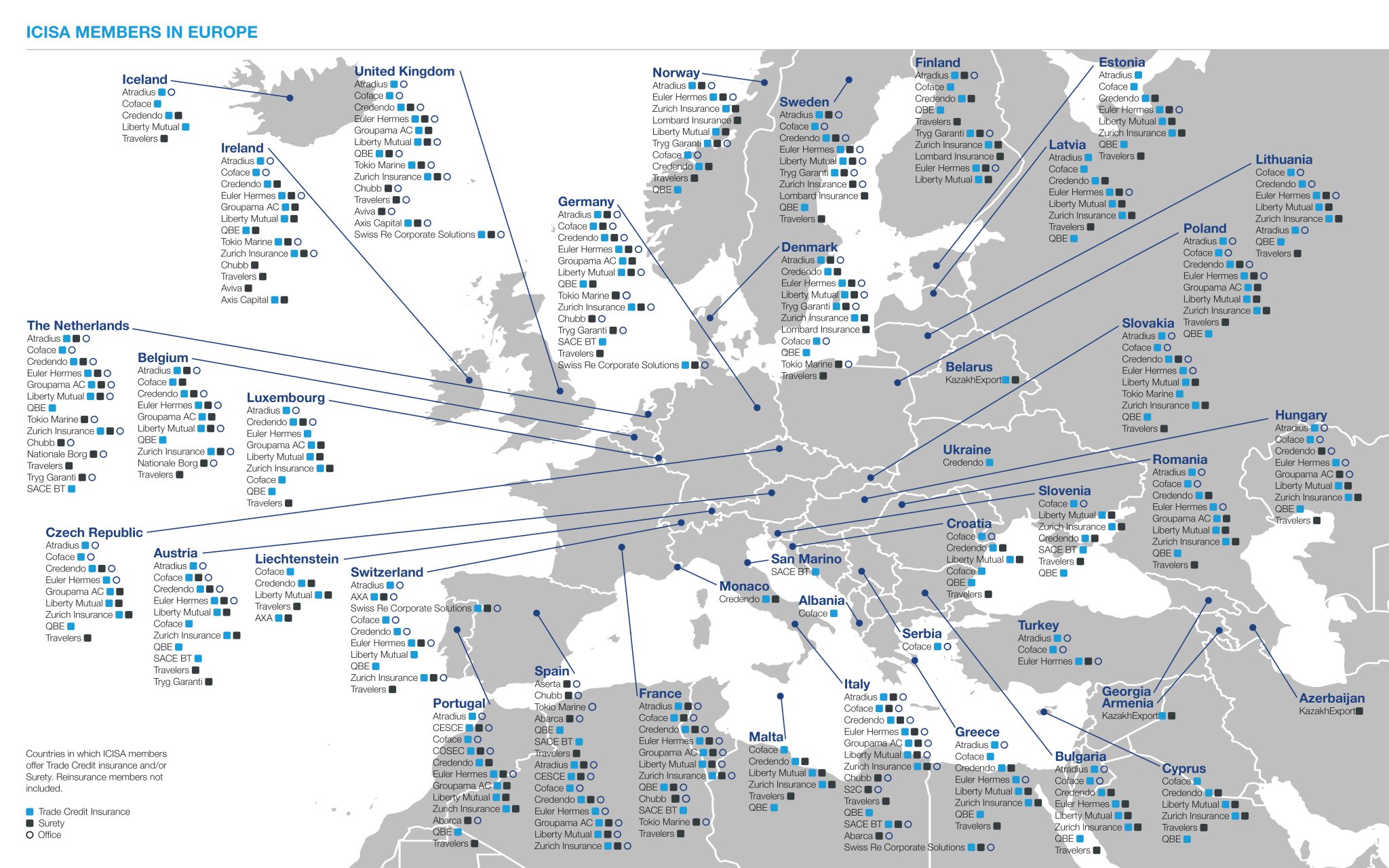

Where is Surety available?

Here is an overview of countries where ICISA’s trade credit insurance and surety members offer their products. Click on each picture to see it on better resolution.

Glossary of Surety terms

A surety bond provides assurance to one party that the obligations of another will be met. A surety is a specialist insurer providing this essential security in a range of industries and scenarios.

FAQ

Below you will find frequently asked questions on TCI related topics. If you have any additional questions please feel free to contact secretariat@icisa.org.

Any questions on the topic?

If you want to know more about this topic, feel free to contact us.