Introduction

Digitalization and transparency, paired with strong governance practices, play an important role in improving trade practices. ICISA supports a range of initiatives under this broader theme, including the fair development and adoption of electronic signatures (e-signatures).

This article provides a general overview of the global e-signature environment as an introductory piece in the series on e-signatures. This will be followed by further articles exploring specific obstacles and developments in different regions, as well as broader topics related to digitalization and transparency.

Defining electronic signatures

E-signature is more than just a digital version of a handwritten signature. In addition to boosting the efficiency and reliability of trade, the implementation of e-signatures in trade also aligns with and supports global high-level policy priorities of digitalization and sustainability.

There is, however, no universal definition of e-signatures, although major legal frameworks describe them in closely aligned terms: electronic data or a process that is attached to or logically associated with a record, and that a person uses to identify themselves and to indicate their approval or intent to sign the record.

Regulatory Environment

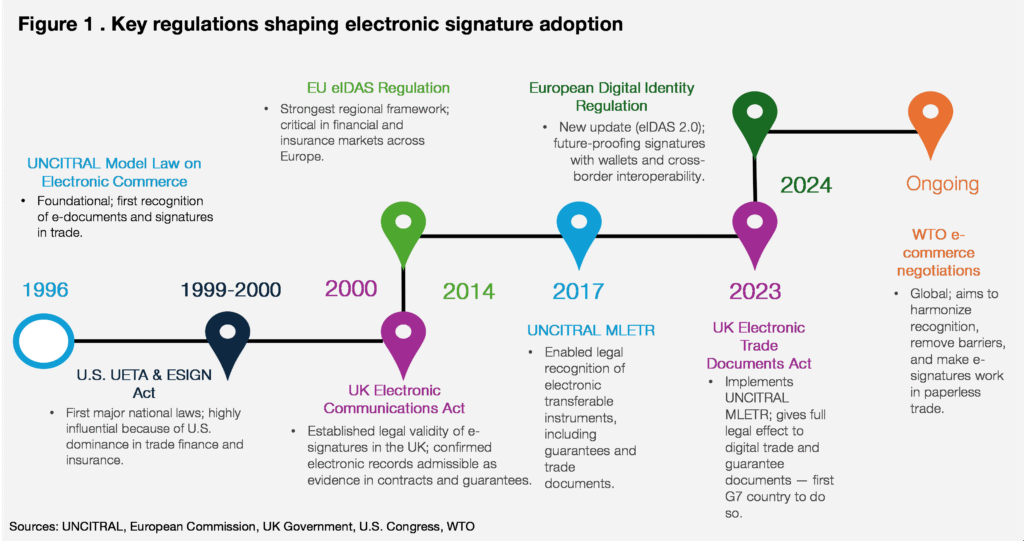

Regulatory frameworks play a decisive role in shaping how e-signatures are accepted and enforced. Global and regional instruments such as the UNCITRAL Model Laws, the U.S. ESIGN Act, the UK Electronic Trade Documents Act (ETDA 2023), and the EU’s eIDAS Regulation all provide the legal foundation for their use in commerce, finance, and insurance (Figure 1).

Together, these frameworks define today’s legal environment for electronic signatures. Yet adoption and interpretation still vary widely across jurisdictions, making mutual recognition and interoperability not just the next frontier, but an essential step toward meaningful reform.

Different regional regulatory traditions continue to influence adoption and recognition. In the United States, the UETA and ESIGN Acts provide long-standing legal certainty, although implementation remains decentralized, with varying state-level acceptance of electronic surety bonds. In the European Union, the eIDAS Regulation (2014) and the forthcoming Digital Identity Regulation (2024) create a trusted cross-border framework, although practical alignment between member states and external partners remains incomplete. In the United Kingdom, the Electronic Communications Act (2000) established e-signature legality, while the Electronic Trade Documents Act (2023) extends full legal recognition to digital trade and guarantee instruments—an important precedent for electronic surety bonds, particularly in the construction sector.

These regional differences directly influence how trade credit insurance and surety markets can leverage e-signatures in practice.

Implications for TCI and Surety

For trade credit insurers and sureties, the impact of e-signatures is significant. Starting with benefits, e-signatures streamline contract execution for policies, guarantees, and reinsurance agreements; reduce administrative costs; enable faster issuance; and align with ESG objectives through paperless workflows. They also reinforce legal certainty where recognized and ensure business continuity through remote execution.

However, the challenges remain. While e-signatures are legally permitted in most markets, the results of a recent survey of Surety members we conducted indicate that their acceptance and practical use are still uneven (e.g. legal validity does not automatically translate into acceptance in practice). High-value transactions, such as large surety bonds or reinsurance treaties, often require enhanced assurance levels (e.g., Qualified Electronic Signatures in the EU, the highest of several legally defined levels under the eIDAS Regulation), adding cost and complexity. Interoperability gaps between platforms (software tools or services such as DocuSign or Adobe Sign used to create, send, and store electronic documents) and certificate authorities (trusted entities such as InfoCert or SwissSign that issue and verify digital certificates) also hinder seamless multi-party execution among insurers and reinsurers.

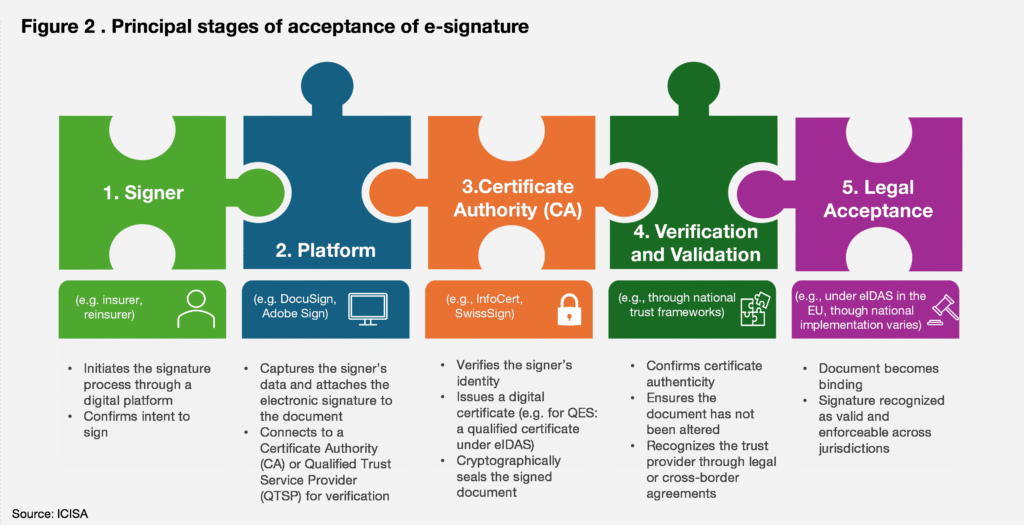

The process of how an electronic signature is created, verified, and ultimately accepted is shown in Figure 2.

To realize the benefits of e-signatures fully, harmonization and mutual recognition are essential; education of stakeholders, supported by secure and resilient systems, will be an important part of this process. Achieving interoperability across trust frameworks and digital identity systems will be key to unlocking efficiency, certainty, and sustainability in cross-border risk transfer. E-signatures aren’t just about signing policies but a pillar of the digital trade infrastructure.

ICISA continues to engage with policymakers advocating interoperable digital trust frameworks that enable the secure and universal acceptance of electronic signatures for surety and trade credit insurance worldwide, supporting the broader digitalization of trade processes such as electronic trade documents as e-bills of lading or electronic customs bonds.

Sources:

- European Commission – What is eSignature?

- UNCITRAL – Model Laws and Conventions on Electronic Communications

- World Bank – Electronic Signatures in Trade Facilitation

- European Commission – Instructions for Qualified Electronic Signatures (QES)

- UNCTAD – Digital Trade Facilitation and Paperless Trade Implementation

- UK Government – Electronic Trade Documents Act 2023