Introduction

In both the EU and the US, rejection of electronic signatures (e-signatures) occurs either by choice or by constraint; the difference is that in the EU these rejections persist because acceptance is not effectively enforced, while in the US they persist because acceptance is not legally required and remains largely subject to market discretion.

This article is the second in ICISA’s Global overview of electronic signatures in Trade Credit Insurance (TCI) and Surety, following the earlier focus on the EU market. It turns the spotlight to the US surety market, one of the largest and most developed globally, characterised by a long-standing and well-defined legal framework for e-signatures. Despite this legal clarity, e-signatures are still not consistently accepted in practice across the US surety and TCI landscape. This raises an important question: where does non-acceptance stem from in a market where the law has recognised e-signatures for over two decades?

Regulatory environment of e-signatures in the US

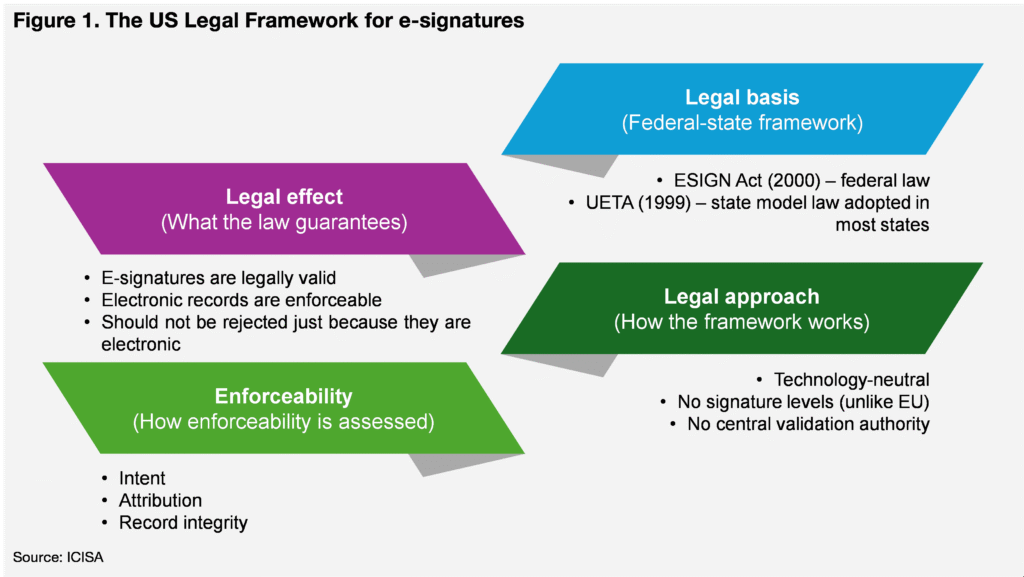

The US legal framework for e-signatures is based on the federal Electronic Signatures in Global and National Commerce Act (ESIGN Act, 2000) and the Uniform Electronic Transactions Act (UETA, 1999). Together, these statutes provide long-standing legal recognition of electronic signatures and records across commercial transactions, including insurance and surety, where the parties have agreed to transact electronically and the transaction is not otherwise excluded by law.

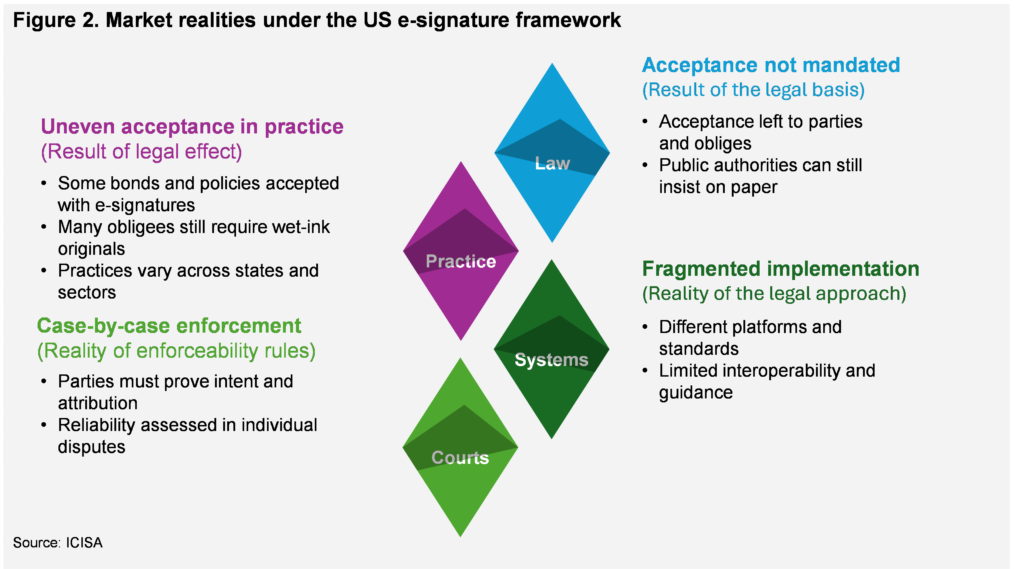

ESIGN and UETA apply broadly, including surety bonds and TCI documentation. The US system lacks a centralized validation framework, and there is no equivalent to the EU concept of qualified electronic signatures. This results in a limited regulatory role in mandating acceptance, leaving implementation largely to contractual terms and market practice. While e-signatures have been legally valid for over two decades, acceptance remains discretionary. This has led to fragmented adoption, with practices varying across states, public authorities, and project owners, despite the clear legal foundation (Figure 1).

While ESIGN and UETA ensure legal validity and enforceability, they do not mandate universal acceptance. At the core of the US approach is a non-discrimination principle, meaning an electronic signature should not be denied legal effect solely because it is electronic, provided the parties have consented to the use of electronic signatures and the transaction falls within the scope of the legislation. The framework is technology-neutral and does not classify signatures by levels, unlike the EU’s eIDAS regime. Enforceability is therefore assessed individually, based on intent to sign, attribution, and the integrity and retention of the record (Figure 2).

Recent court cases show that increased digital adoption has exposed gaps between legal frameworks and practical use. In other words, digitization has revealed ambiguities, prompting courts to provide clarification. This demonstrates that digital progress is driving the need for legal updates—to reduce ambiguity, limit reliance on case-by-case rulings, and enable broader adoption. As part of that effort, narrowing the discretionary space that currently allows e-signature rejection is crucial. Doing so supports both a more efficient US surety market and broader policy goals around digital transformation and sustainability.

Clarifying acceptance requirements in the US is a key step toward making digital execution the default. This will require tailored legal or policy tools, depending on the reasons behind non-acceptance.

Surety and TCI implications

The US surety market is large: according to data from the Surety & Fidelity Association of America (SFAA), direct premiums written reached about USD 10.7 billion in 2024. It is a mature and operationally conservative segment, especially for high-value or public-sector bonds, which makes continued reliance on wet-ink signatures an even greater hurdle.

The Surety and TCI implications of e-signatures not being accepted often translate into:

- parallel digital and paper workflows that duplicate effort,

- delays in bond and policy issuance,

- increased operational costs and inconsistent acceptance of otherwise fully valid electronic guarantees and policy documents.

Reasons e-signatures get challenged in practice can broadly be grouped into two categories: rejection by choice and rejection by constraint. Rejection by choice is mostly driven by habit, legal conservatism, perceived litigation or fraud risk, and internal policies that have not yet been updated to reflect the legal validity of e-signatures. Rejection by constraint is mainly the result of legacy systems, limited interoperability between platforms, prescriptive internal procedures, or procurement and court processes that have not yet been redesigned for digital execution. Understanding this distinction is essential for designing targeted solutions.

Addressing the challenges

Unlike in the EU, non-acceptance in the US is largely shaped by market behaviour and legacy expectations. Acceptance decisions are frequently left to obligees or project owners, which limits the ability of sureties to influence execution requirements and means that many refusals fall into the “rejection by choice” category.

A useful starting point for addressing these challenges is to distinguish clearly between the motives behind rejection: is it driven by conservative practice, internal policy and habit (rejection by choice), or by system limitations, record-keeping gaps, lack of audit trails and similar constraints (rejection by constraint)? Improving market confidence then means strengthening internal standards for authentication, identity verification and auditability, and clearly documenting e-signature processes and their evidentiary reliability. It is equally important to promote awareness that ESIGN and UETA already provide legal enforceability, and that paper does not inherently reduce legal or fraud risk – a message ICISA consistently supports.

Furthermore, industry-led guidance and best practice standards should be encouraged, rather than a wholesale regulatory overhaul. Recent developments in the US surety market show that this shift is already underway. In late 2025, four major surety providers – Chubb, The Hartford, Liberty Mutual and Travelers – jointly announced the launch of SuretyBind, a technology company intended to provide shared digital infrastructure for the market, including a data transmission platform and digital bond execution. By streamlining bond issuance, improving verification and reducing fraud risk, initiatives such as SuretyBind illustrate how industry-driven solutions can help translate the legal validity of e-signatures into more consistent acceptance in practice.

E-signature adoption is fully aligned with high-level policy goals on digitalisation and sustainability, and those goals are set to be achieved, not ignored.

ICISA positions itself as a platform for sharing best practices, promoting more consistent acceptance standards, and supporting members in transitioning away from legacy paper-based processes. There is already growing momentum from digital bond initiatives and platform development in the US, even as electronic signatures remain uneven in practice, and ICISA will continue to advocate for and support improved industry practice.