What are Public Guarantee Schemes

Public Guarantee Schemes (PGSs) are publicly backed guarantee instruments used worldwide to support economic goals aligned with national or supranational policy priorities. They are widely used to advance policy objectives such as SME financing, infrastructure development, innovation, and the green and digital transitions. PGSs are also deployed in response to major crises, including pandemics and geopolitical disruptions.

What is their purpose

Their primary purpose is to mobilize private capital by providing additional support that encourages financial institutions to lend or invest in targeted areas. They do this by acting as a risk mitigant for these institutions (typically banks), thereby instilling the confidence needed to release capital into the real economy. This helps unlock financing for priority sectors or initiatives supporting broader economic and policy goals.

How do Public Guarantee Schemes work

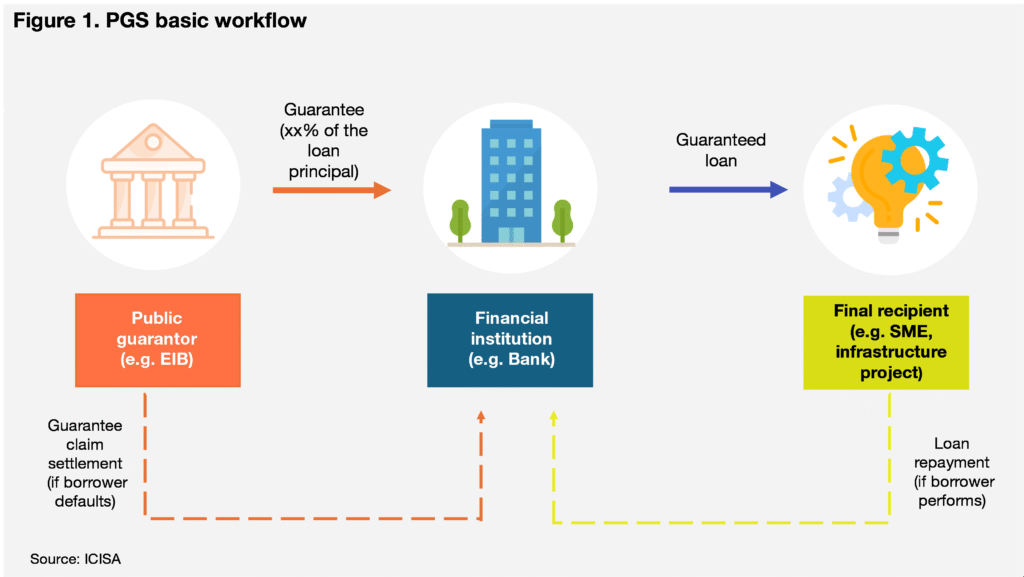

The basic principle of operation is broadly consistent among the schemes. A public guarantor provides a guarantee to a financial institution, most often a commercial bank. This guarantee typically covers a portion (e.g. 50–80%) of potential losses on loans issued to the final user (e.g. SMEs, infrastructure projects), thereby de-risking the transaction for the institution. If the borrower repays, the institution receives full payment with interest. If the borrower defaults on the loan (e.g. project failure), the institution claims the guaranteed portion from the guarantor (Figure 1).

This structure applies across both supranational programs (e.g. InvestEU) and national-level schemes (e.g. KfW, Bpifrance), adapting to different policy priorities but following the same underlying logic. While guarantees are typically provided indirectly via financial institutions, some schemes also allow direct guarantees to be issued to the final beneficiary, and may, depending on the design and policy objective, engage non-traditional financial actors such as alternative finance platforms as intermediaries.

Who provides Public Guarantee Schemes

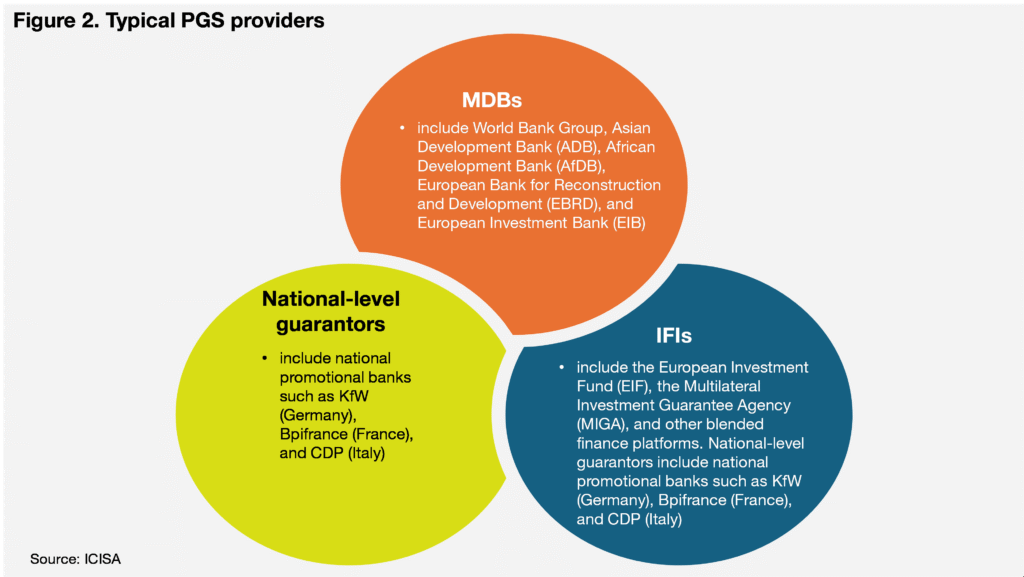

Public Guarantee Schemes are typically provided by Multilateral Development Banks (MDBs), International Financial Institutions (IFIs), and national-level public guarantors (Figure 2).

What form do they usually take

While approaches vary, PGSs are commonly structured along a few key dimensions including the source of funding, the level at which risk is shared, and whether coverage applies to individual transactions or portfolios. These design features are typically adapted to the policy objectives, market needs, and delivery mechanisms of each scheme.

How do the insurers fit in

PGSs are emerging as a potential source of new opportunities for the credit and surety sector. As governments look to stimulate investment and crowd in support from traditional financial services, these schemes are likely to grow in importance, offering new avenues for insurers to engage in policy-driven finance.

So far, the primary financial institution between public guarantors and final beneficiaries has been the largest player: the bank. However, in today’s environment of heightened uncertainty and elevated risk, the role of financial actors beyond banks (including pension funds, investment funds and finance companies, among others) as a supplementary channel is gaining prominence, particularly among those positioned to support targeted, policy-aligned economic activity.

These actors now account for nearly half of the global financial assets. According to the Financial Stability Board (2024), this segment of the financial system grew by 8.5% in 2023, more than double the growth rate of the banking sector. Within this landscape, insurance companies that represent a significant share (~20%) are well placed to play a greater role in PGSs. For example, sureties can provide performance bonds that are counter-guaranteed by the PGS. It is also important to recognize that insurance operates under distinct prudential regimes and plays a unique role in risk mitigation, separate from other NBFI activities.

Alternatively, credit insurers can support PGSs indirectly by providing security for a PGS rather than guaranteeing the PGS itself. For example, trade credit insurance (TCI) can be used to cover SME receivables, improving the credit profile of borrowers. This risk mitigation, when combined with public guarantees, can make borrowers more attractive to private financiers and enhance access to credit.

ICISA members represent 95% of the global private credit insurance market, covering nearly €3.2 trillion in trade receivables and billions in infrastructure guarantees. TCI and surety, as risk mitigation and capital relief tools, already align with the objectives of PGSs.

With appropriate recognition by public authorities of the value of credit insurance and surety, insurers could offer these already aligned products with greater confidence and expanded reach, particularly in areas that support EU-level priorities. For more on how TCI and surety relate and contribute to these priorities see the article Bridging Digitalization and Green Transformation: Clean Tech, TCI and Surety.

ICISA has held positive initial conversations with a number of institutions behind PGS arrangements to discuss ways to broaden participation in these to include insurers. While discussions are still at an early stage, this reflects ICISA’s commitment to expanding its members’ role in supporting strategic economic objectives.